We’ve conducted extensive backtests using a range of entry and exit thresholds on the major U.S. indices. By leveraging historical index data (instead of ETFs like SPY), we’ve been able to analyze performance across a much deeper historical timeframe.

Is the backtest robust?

The short answer: YES.

This model is inherently robust, with no parameters to optimize beyond the entry and exit thresholds. Seasonal patterns, such as Christmas occurring in late December or July always having 31 days, are fixed and unchanging. These predefined timings eliminate the need for parameter optimization, reducing the risk of overfitting and ensuring the model’s reliability.

ETFs

Backtests on the major US ETFs.

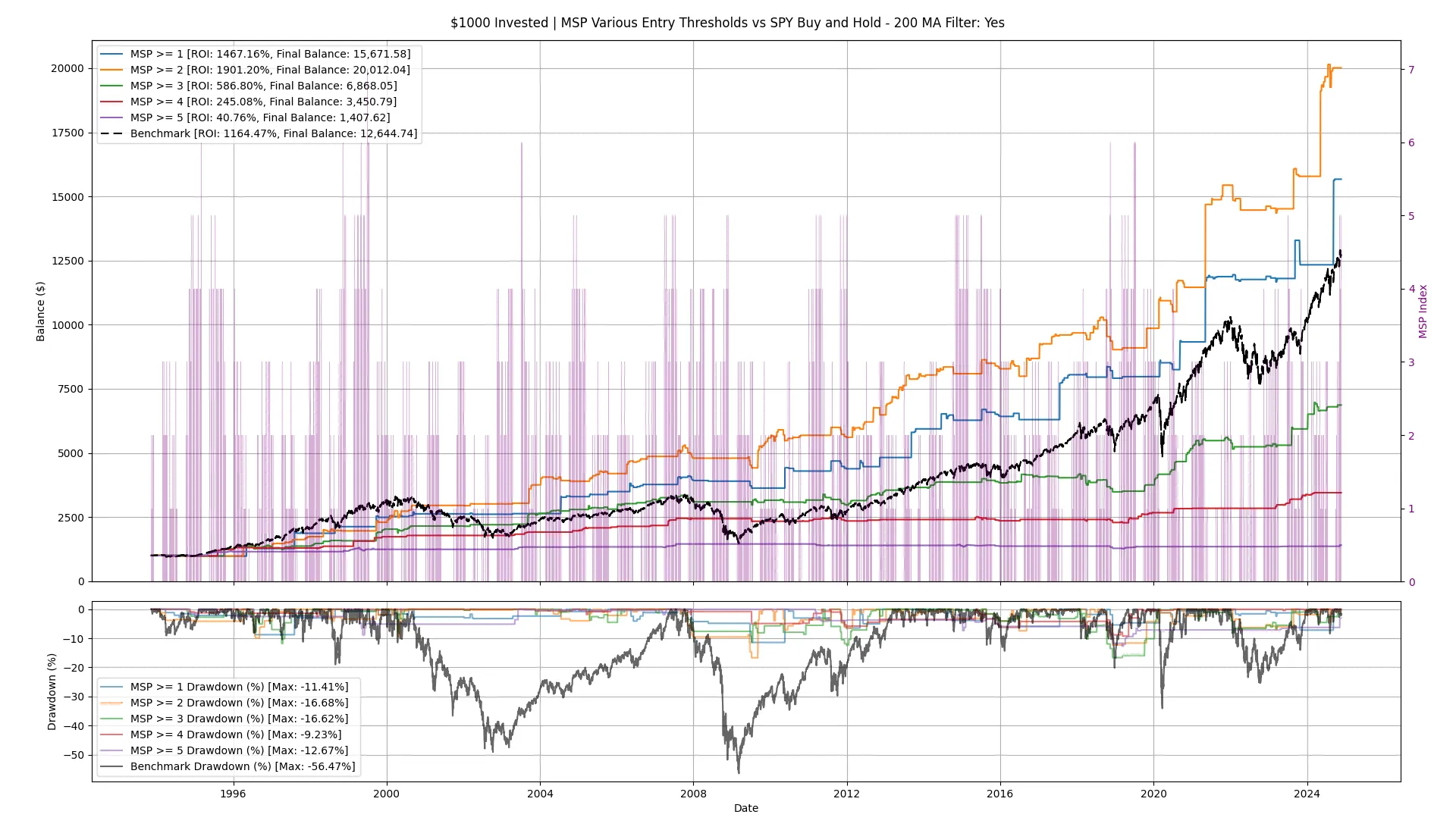

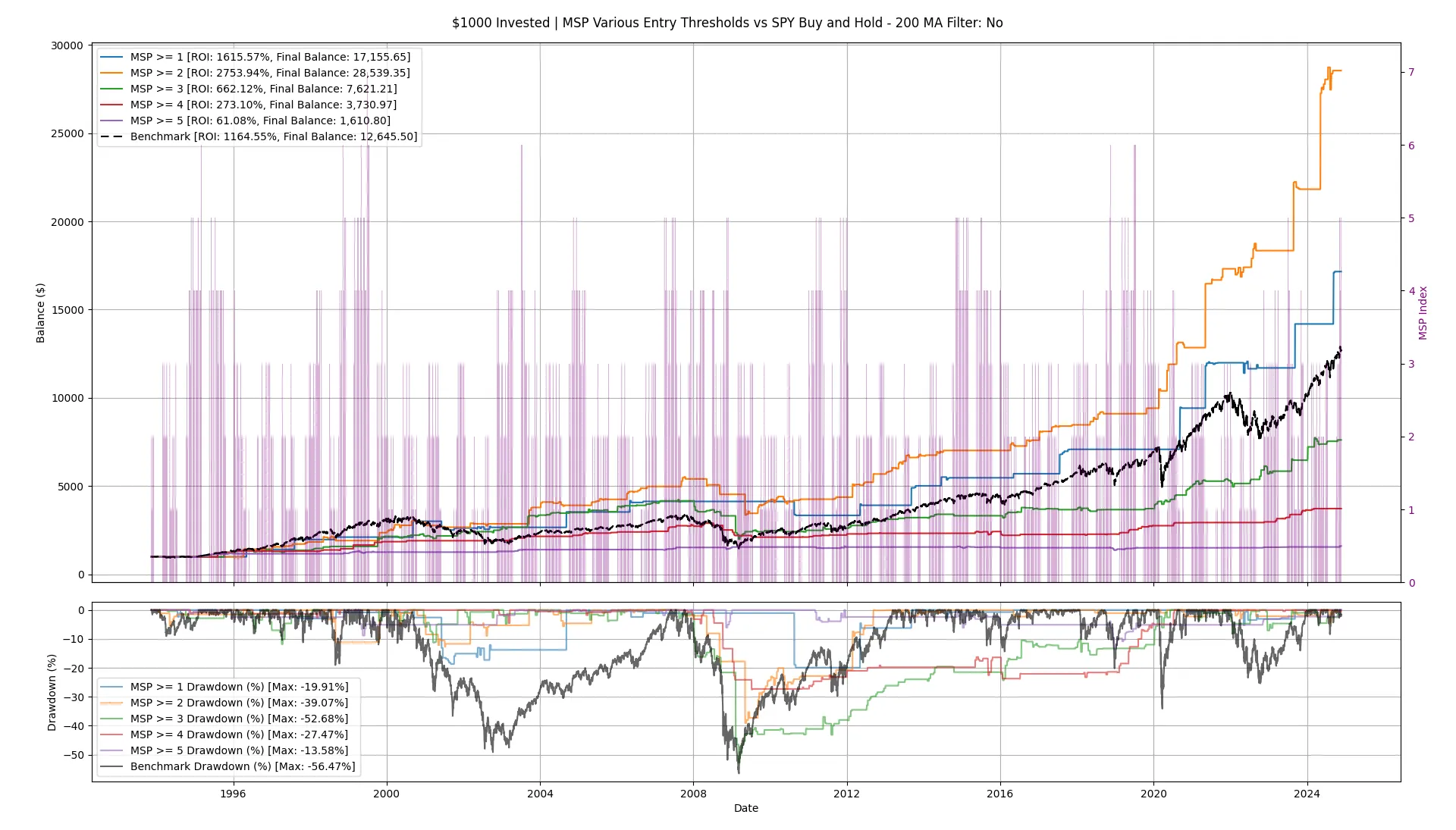

SPY

RULES

Entry/Long: when MSP index >= given threshold

Exit/Cash: when MSP index < given threshold

200 MA Filter: Yes

SPY

RULES

Entry/Long: when MSP index >= given threshold

Exit/Cash: when MSP index < given threshold

200 MA Filter: No

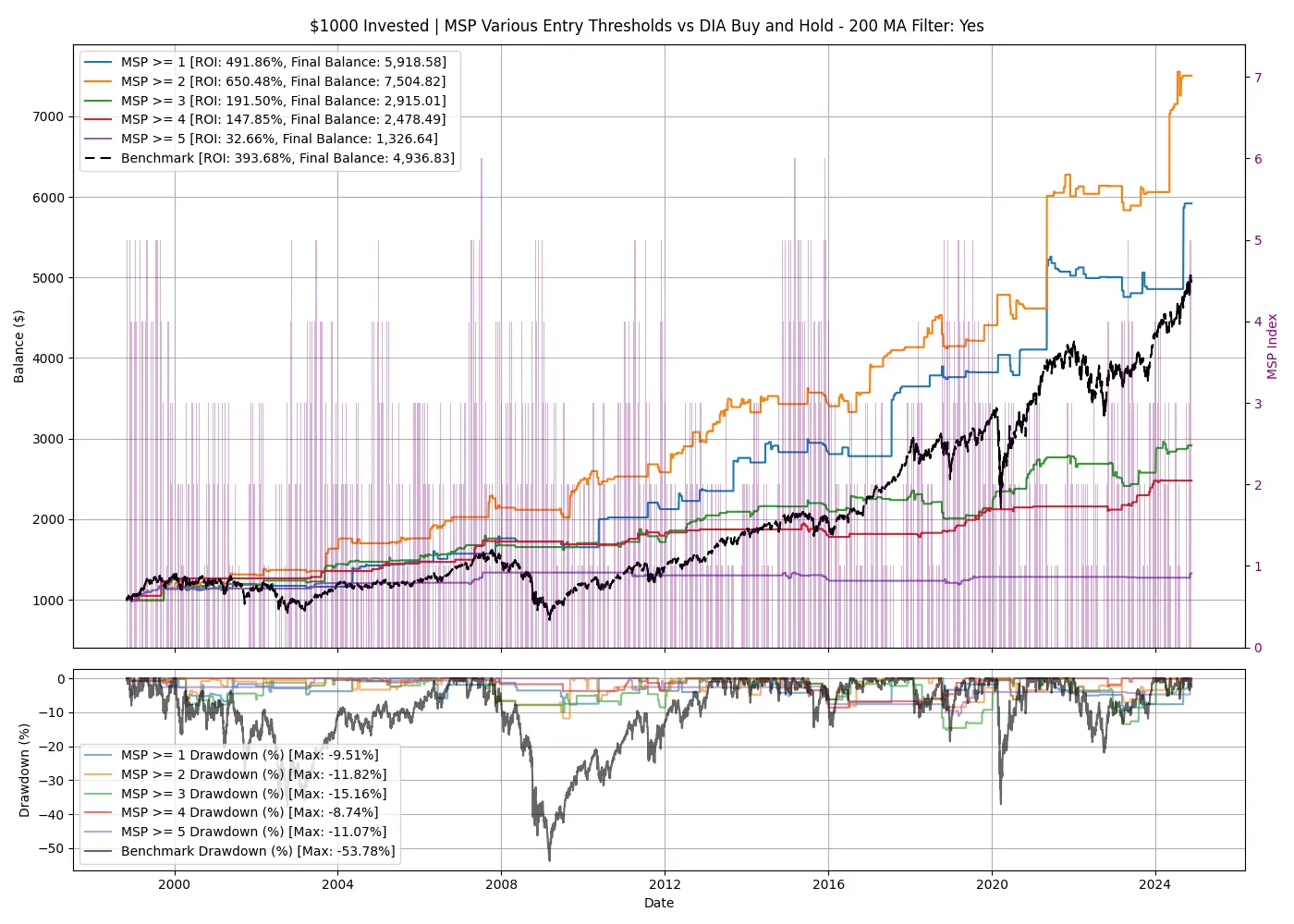

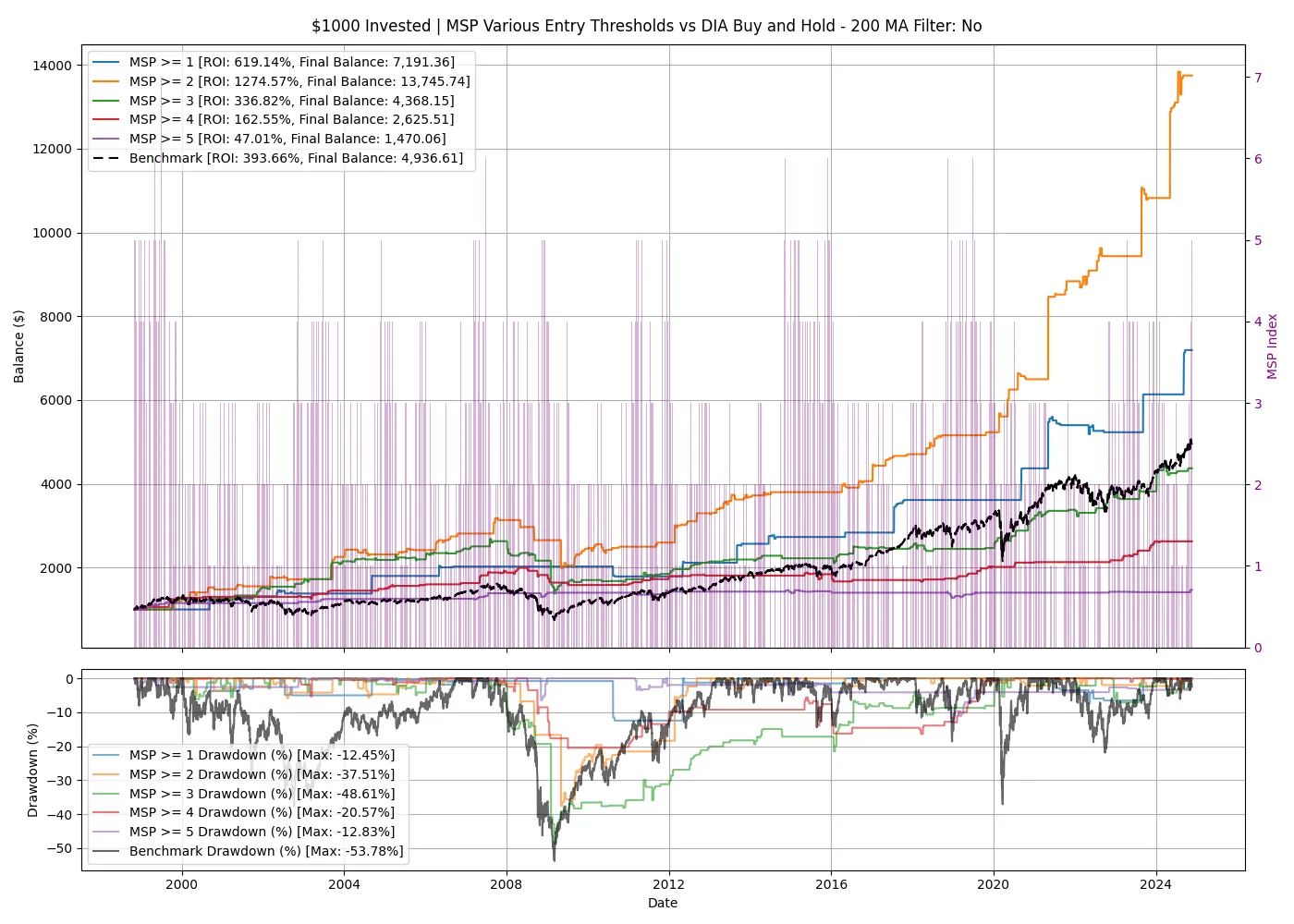

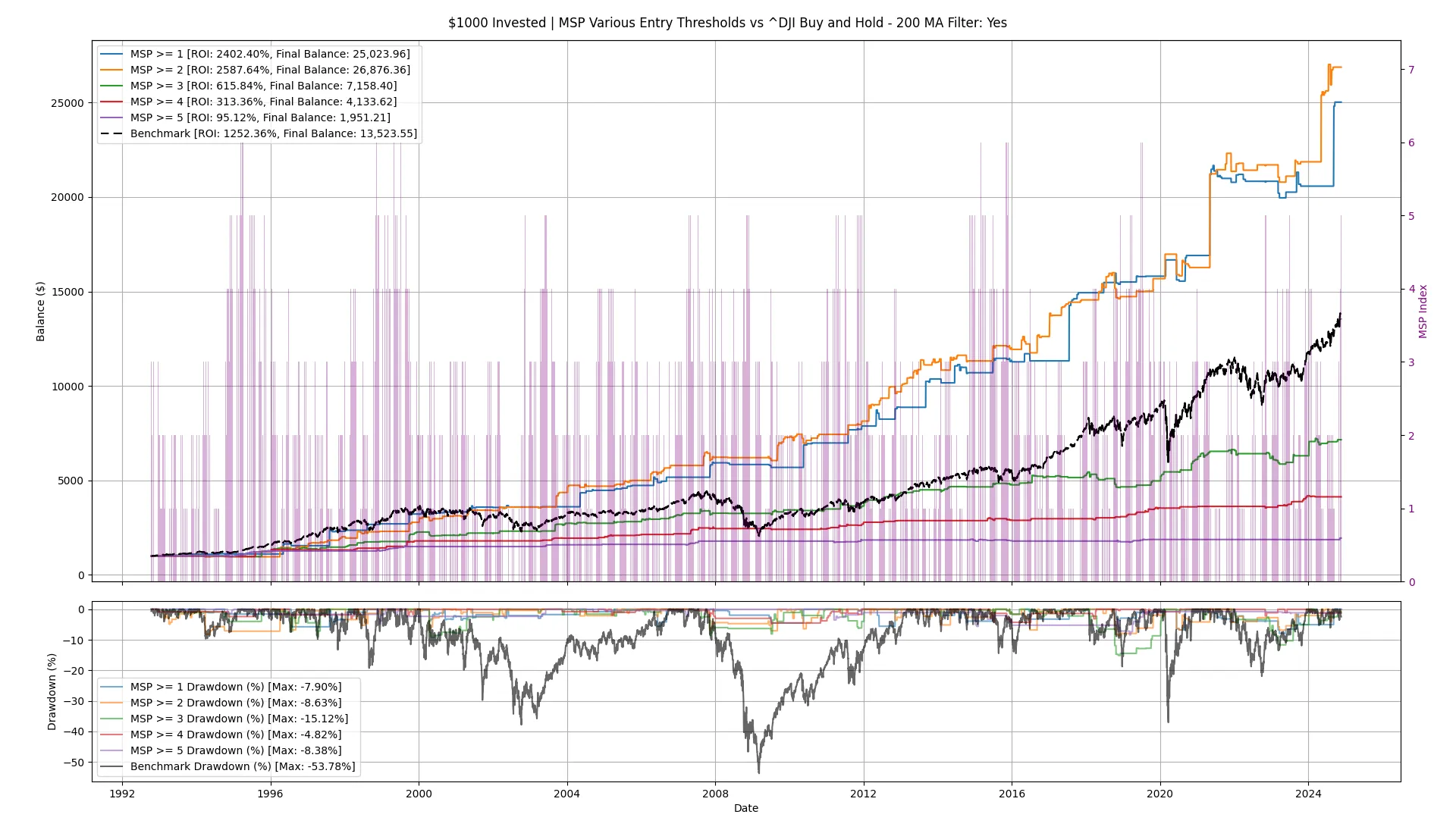

DIA

RULES

Entry/Long: when MSP index >= given threshold

Exit/Cash: when MSP index < given threshold

200 MA Filter: Yes

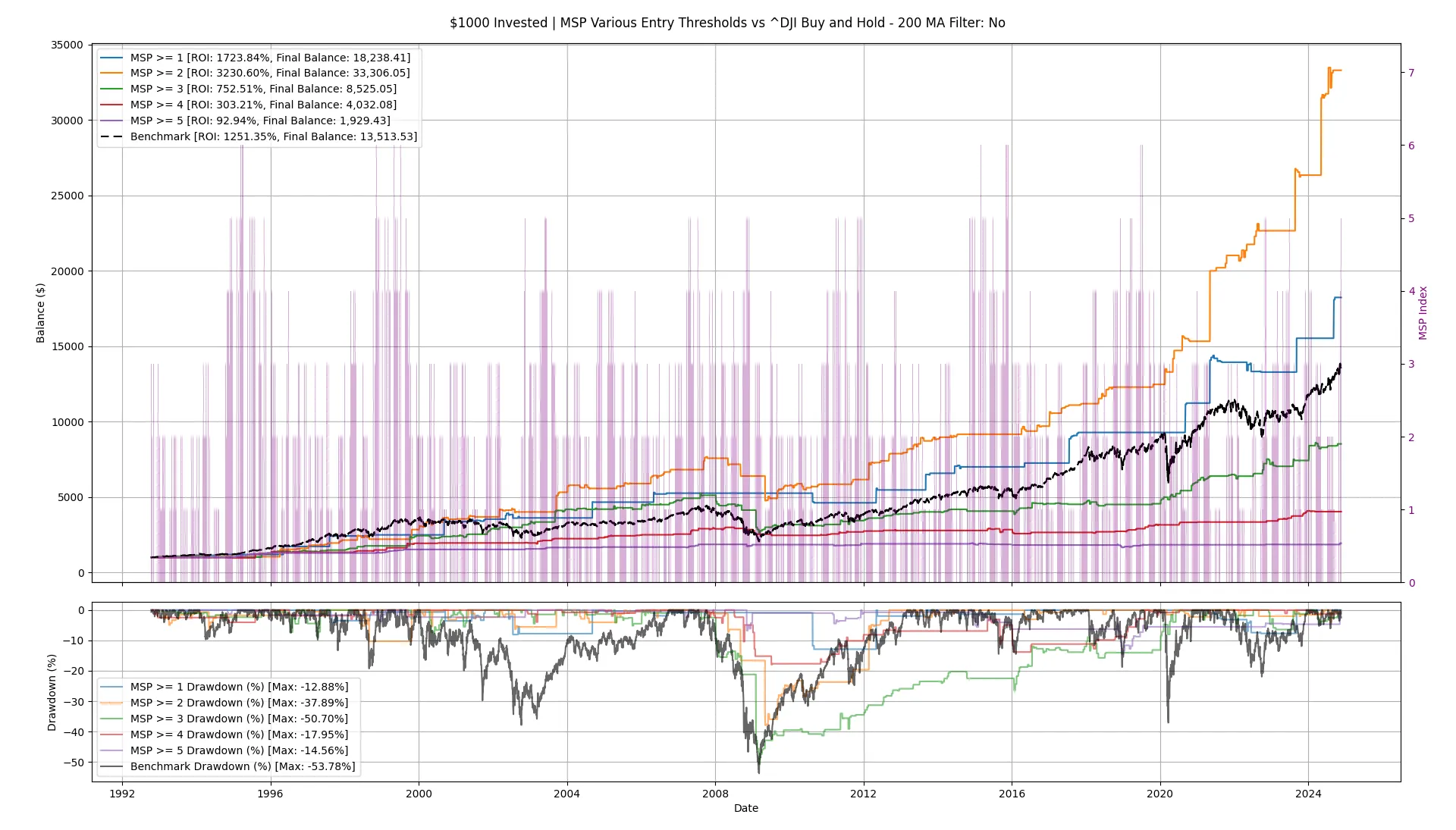

DIA

RULES

Entry/Long: when MSP index >= given threshold

Exit/Cash: when MSP index < given threshold

200 MA Filter: No

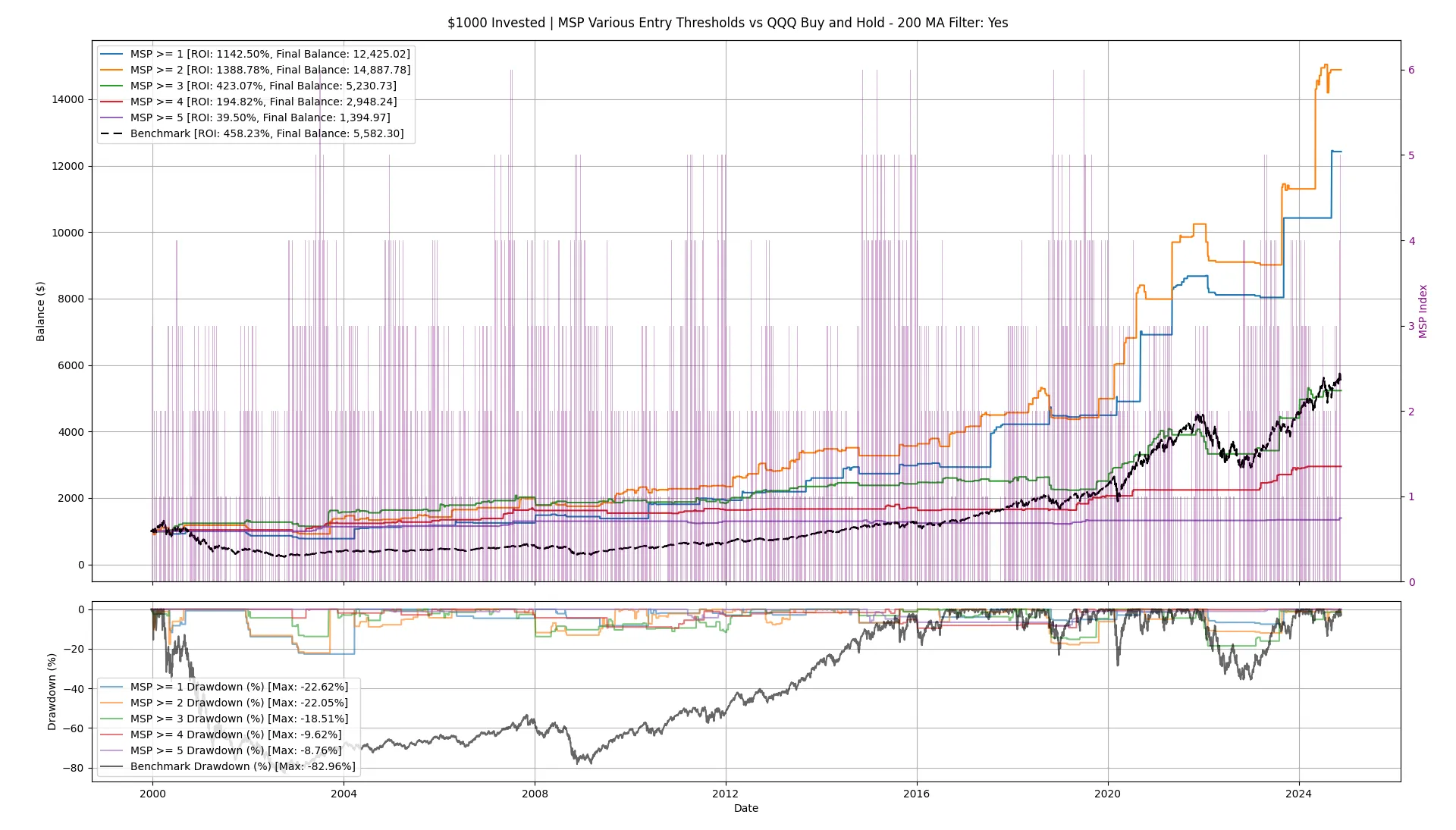

QQQ

RULES

Entry/Long: when MSP index >= given threshold

Exit/Cash: when MSP index < given threshold

200 MA Filter: Yes

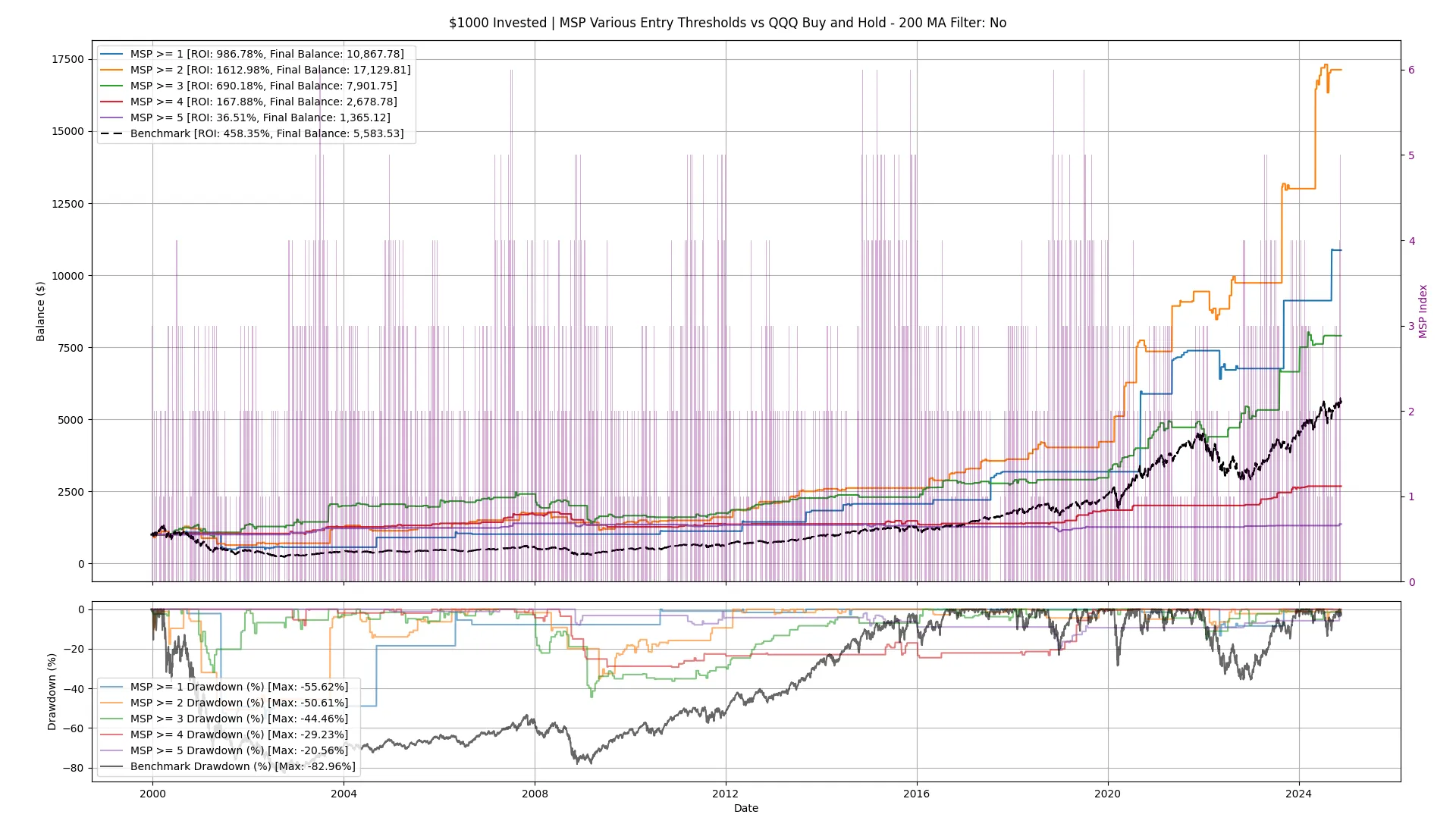

QQQ

RULES

Entry/Long: when MSP index >= given threshold

Exit/Cash: when MSP index < given threshold

200 MA Filter: No

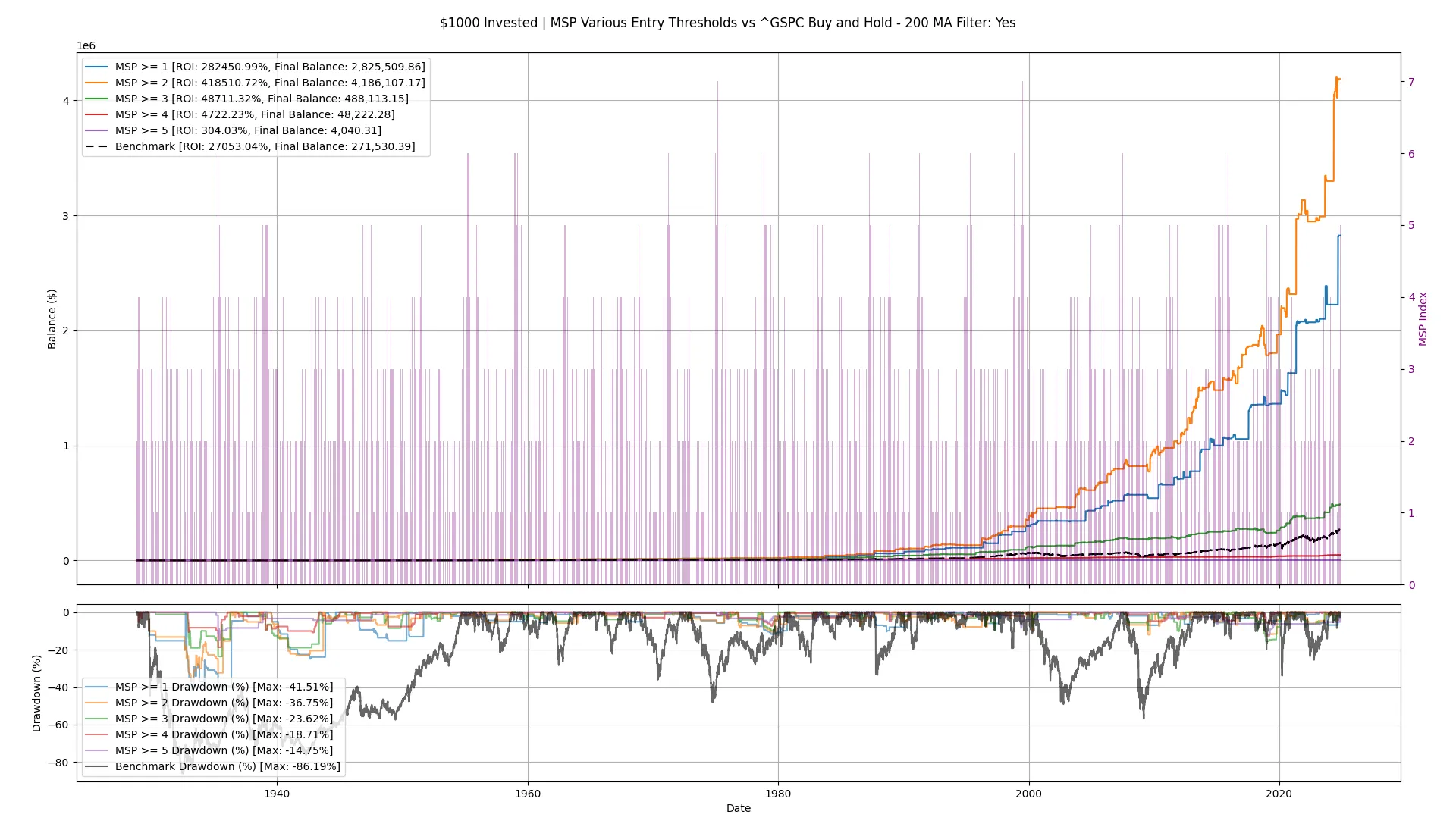

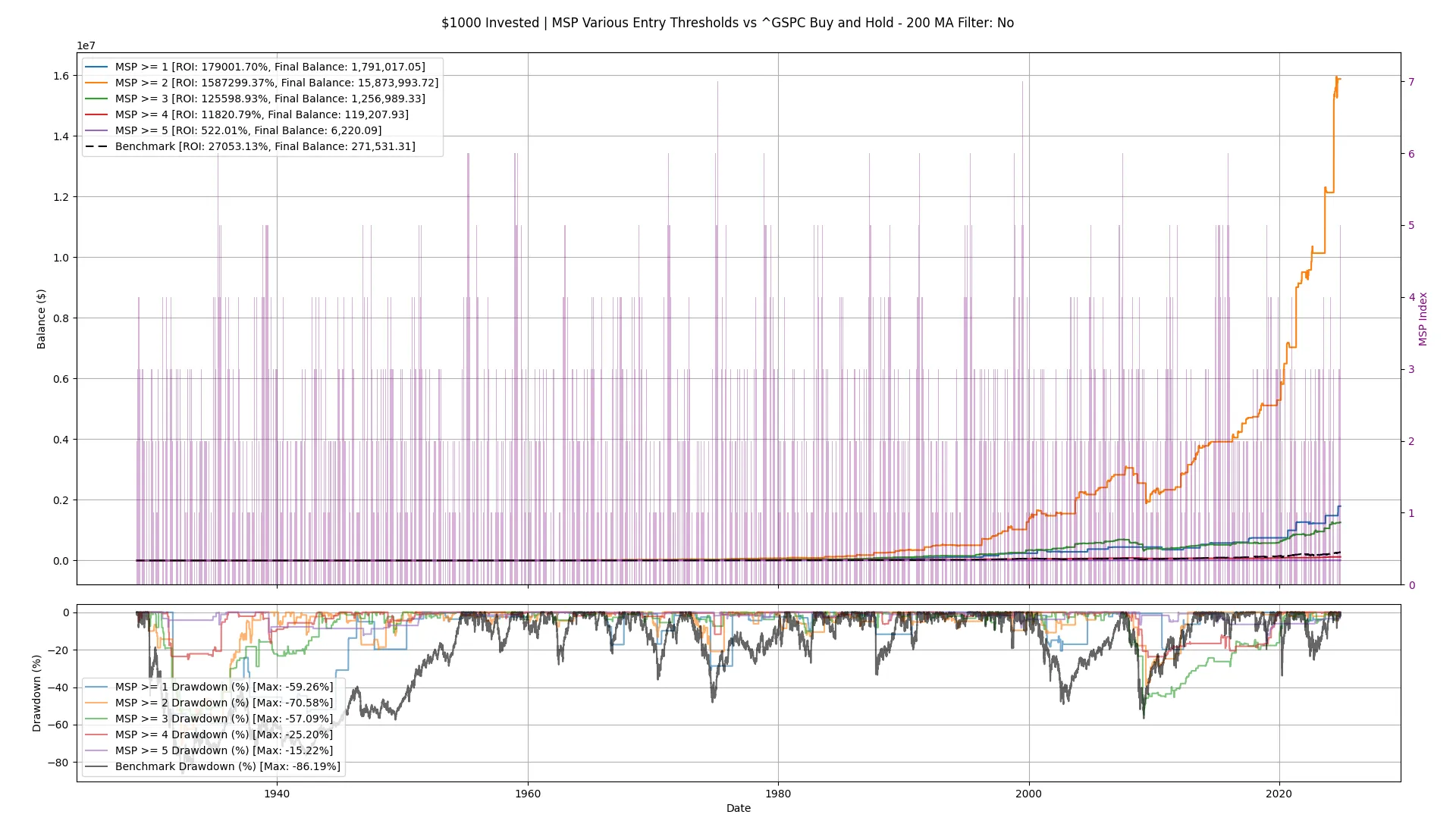

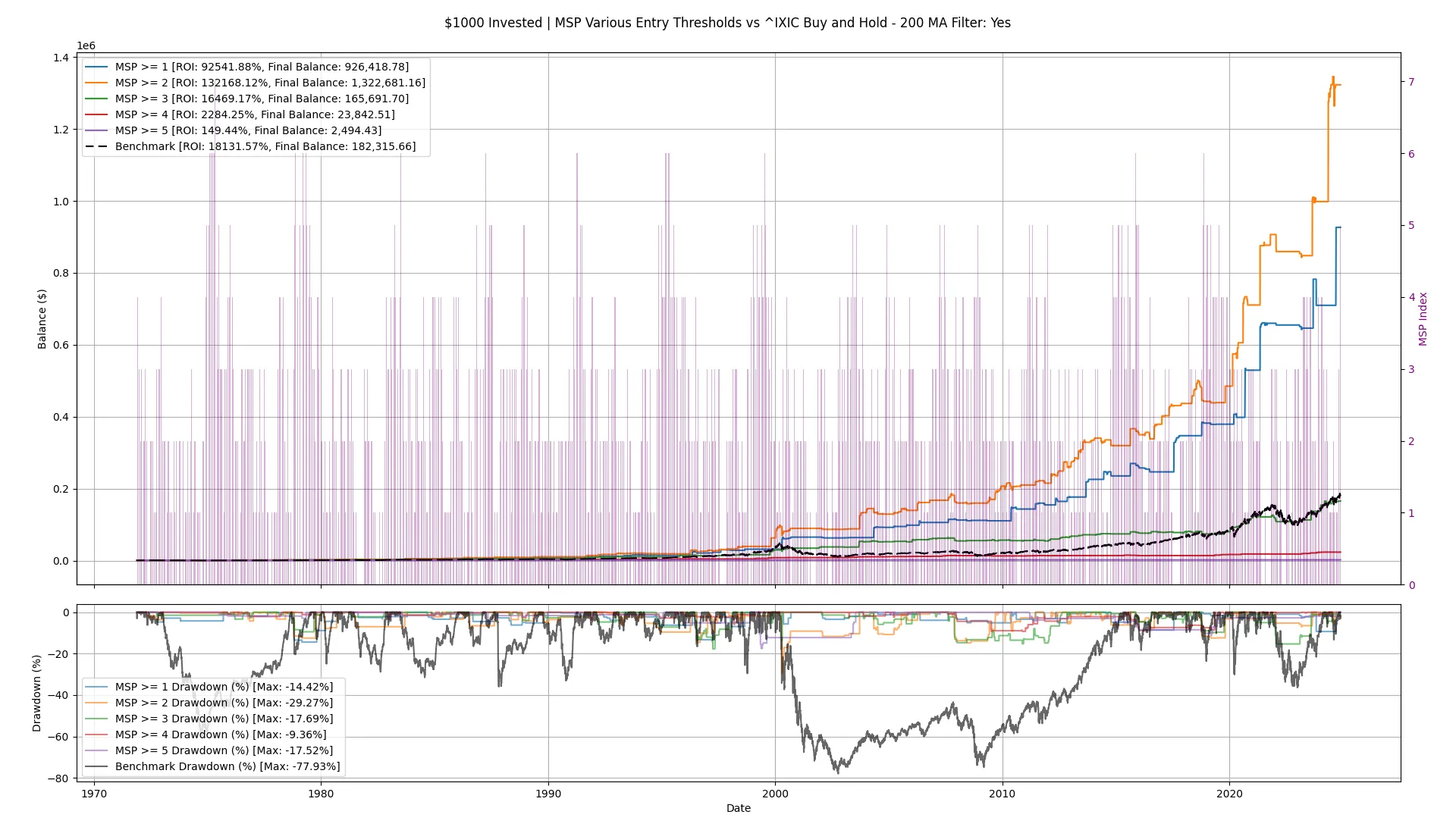

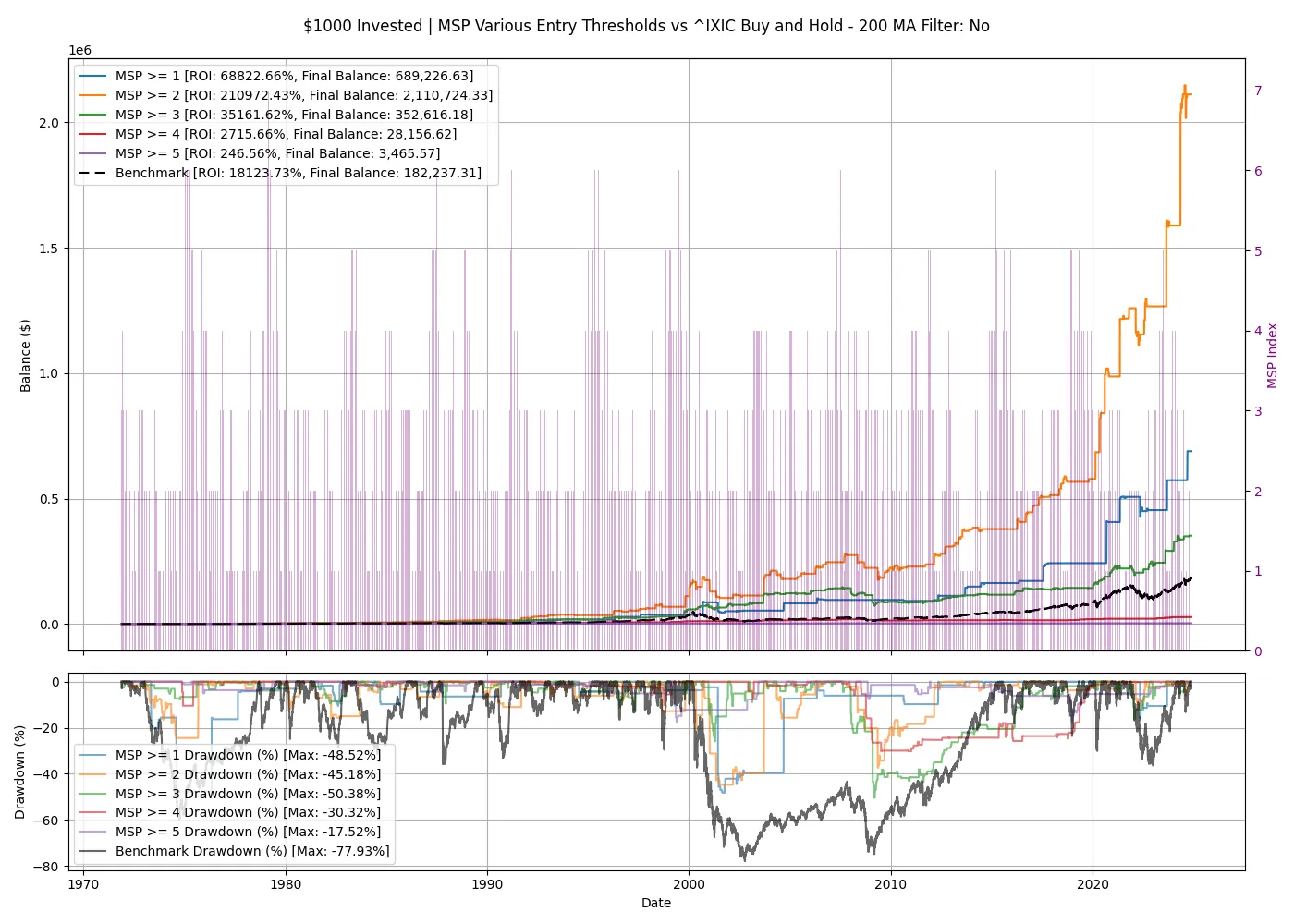

INDICES

Below are backtests conducted directly on the index, leveraging its longer historical data for analysis instead of the ETF.